As Miriam Gottfried wrote in the Wall Street Journal last month, “wealthy Americans are buzzing about donor-advised funds (DAFs), and the surge in adoption that started at the end of 2025 has continued into 2026.”

We can confirm that momentum is real. 2025 was a huge year for Daffy, and 2026 looks to be even bigger. What the coverage tends to miss is that DAFs aren't just for the ultra-wealthy. The reason that group discovers them first is simple: they have financial advisors.

Throughout the year, advisors sit down with their clients and help unlock thousands of dollars in tax savings through a handful of strategies most people have never heard of. Not surprisingly, the donor-advised fund is at the center of many of them.

We recently put together a presentation for financial advisors at Betterment (read about our partnership with Betterment on stock donations) that walks through exactly when and why they recommend a DAF. However, you don’t need to be a financial advisor to understand the most common scenarios when a donor-advised fund can add significant value to your financial life.

Here are four situations where a donor-advised fund can unlock incredible tax savings.

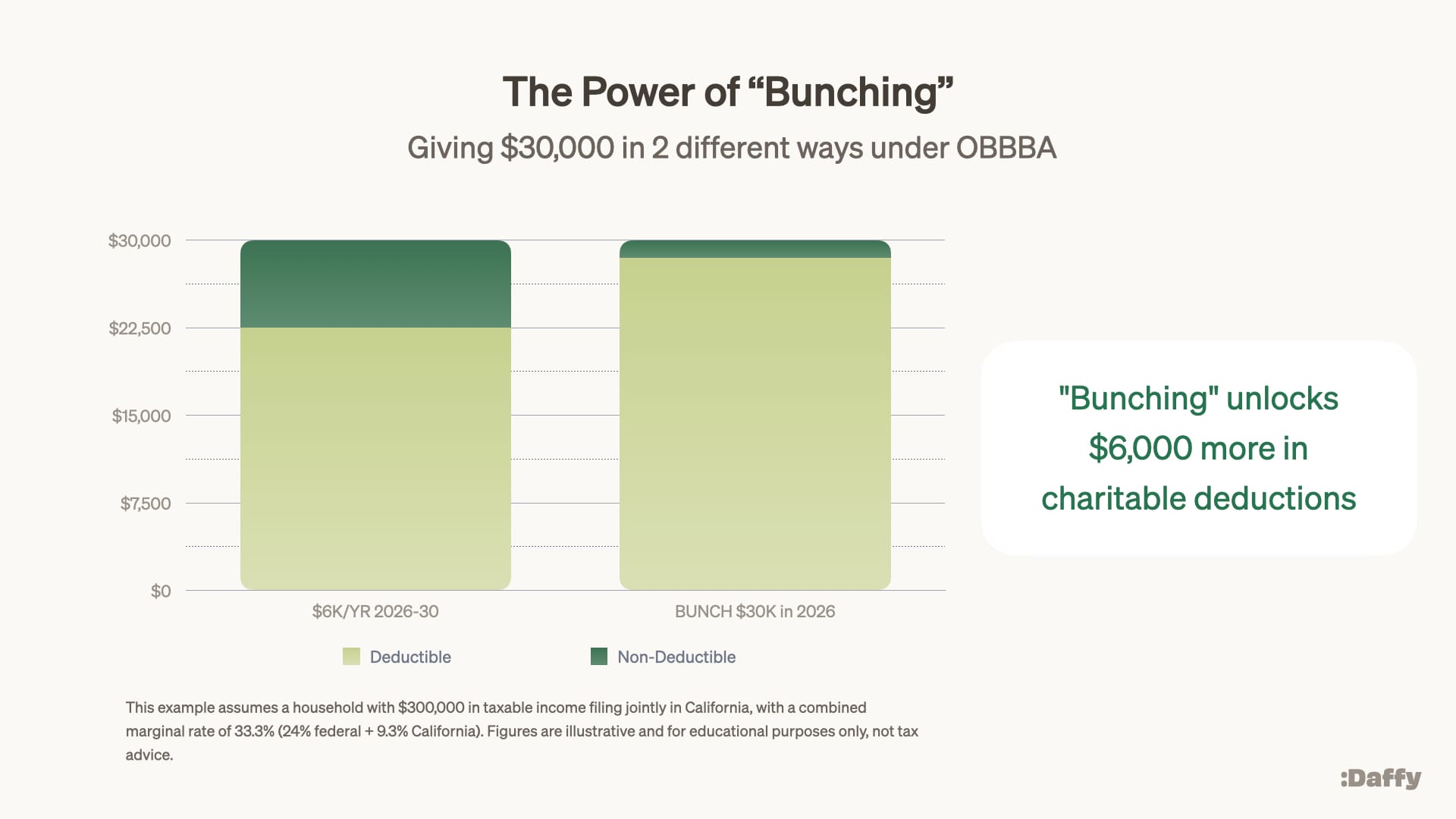

1. You want to give more, but your donations aren't moving your tax bill

The 2017 Tax Cuts and Jobs Act nearly doubled the standard deduction, and for a lot of generous people, that quietly made their charitable giving tax-invisible. If you're giving $5,000–$15,000 a year but not clearing the itemization threshold, you're not getting the tax benefit you wish you could.

The strategy advisors use is called bunching. Instead of giving $6,000 every year, you contribute a few years' worth into a DAF in a single tax year. That larger contribution clears the threshold, unlocks the deduction, and you still can donate to your favorite charities on whatever schedule you like.

The giving doesn't change, the tax outcome does.

As Chris Arnold, CFP of Refresh Wealth says, “Pre-funding donations into one tax year can push your total donations over the standard deduction and make it where itemizing your deductions becomes attractive.”

The One Big Beautiful Bill Act (OBBBA), passed in 2025, introduced a new floor: you can only deduct charitable donations that exceed 0.5% of your annual gross income (AGI). Now, 0.5% doesn’t sound like a lot, but it turns out that, on average, U.S. households give about 2% of their income to charity every year. As a result, that seemingly tiny 0.5% can mean a loss of 25% of your tax deduction!

For a couple with $300,000 in annual gross income, that means only the amount above $1,500 is deductible, whether their total donations are $2,000 or $20,000.

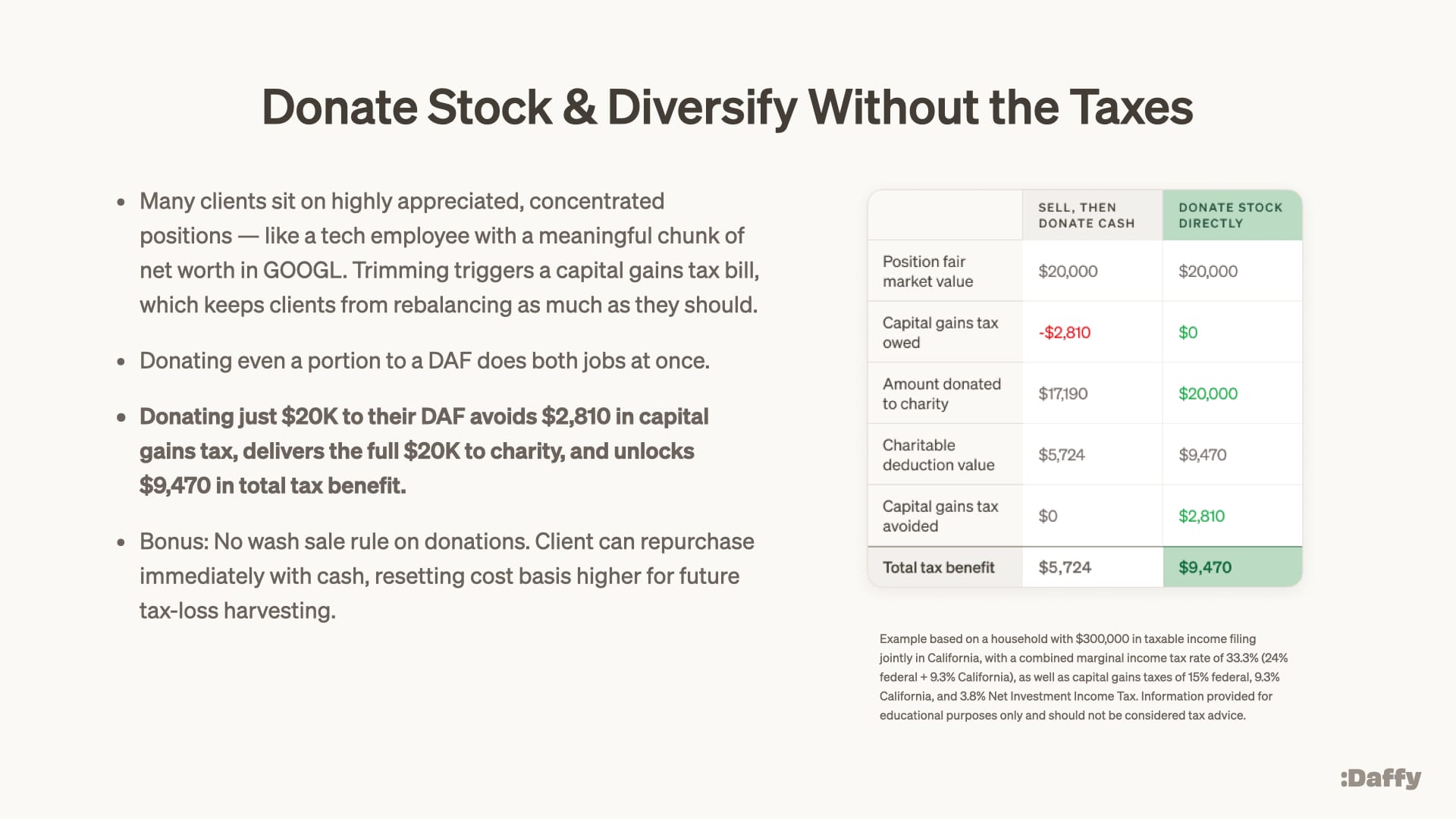

2. You have appreciated stock, ETFs, or crypto — but you’re still donating cash to charity

If you're writing checks or using your credit card to give to charity, you're leaving a lot of money on the table, especially if you're an investor. When you donate appreciated assets like stocks, ETFs, mutual funds, or crypto, you get the full charitable deduction and permanently avoid the capital gains tax you'd owe if you sold first.

Say you give $20,000 a year. If that money is sitting in appreciated securities, donating the shares instead of selling and giving cash could save you thousands on top of the deduction. And here's something most people don't know: unlike selling, donations aren't subject to wash sale rules. You can donate appreciated shares and immediately repurchase the same security, now with a higher cost basis, without any waiting period.

The practical catch is that most charities aren’t set up to accept stock directly, and in some cases, you want to split your donations across multiple organizations. Turns out, a DAF solves for that. You contribute the appreciated assets to your DAF, take the deduction, and then make donation recommendations of any amount to any legal charity you choose on your own timeline.

This is also a great way to trim a concentrated position without triggering a tax bill. For an employee with a significant chunk of net worth in company stock, selling to diversify means paying capital gains taxes, which is exactly why most people don't do it enough.

Instead of selling, donate a fraction of the shares. Donating a portion to a DAF lets you reduce the position and give at the same time, with no capital gains owed.

Donating $20K worth of shares avoids $2,810 in capital gains tax, delivers the full $20K to charity, and unlocks $9,470 in total tax benefit!

3. You have a big year and need a deduction fast

A large bonus. A business sale. An IPO. When a windfall hits — maybe in June, maybe in December — the tax bill can be significant and the window to do something about it is short.

You don't want to rush meaningful philanthropy, and lining up that level of giving to the right organizations in a matter of weeks isn't realistic for most people.

A DAF solves the timing problem by separating putting money aside for charity from the decision of which charity to give it to. Charitable deductions can offset up to 60% of your AGI, making it one of the most generous deductions in the entire tax code.

Say you receive a $100,000 bonus: at a combined rate of 41.3% (32% federal + 9.3% California), that's a $41,300 tax bill. A contribution of up to $60,000 to your DAF before December 31 would be fully deductible, reducing that bill by up to $24,780. And that contribution doesn't have to go out the door immediately, after your contribution, the funds are invested and growing tax-free while you take the time to decide where it would do the most good.

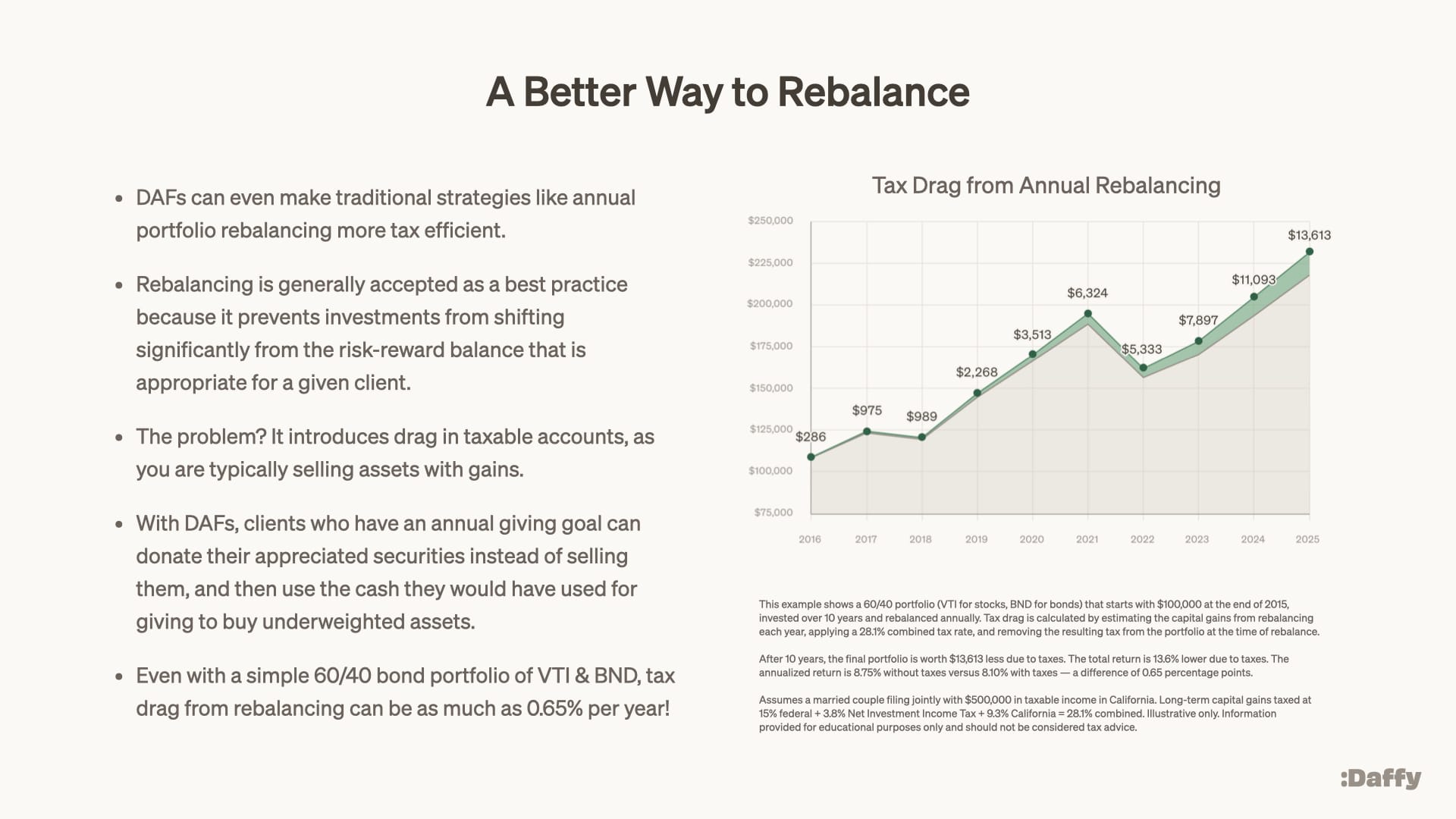

4. You rebalance your portfolio every year and keep triggering capital gains

Rebalancing is widely considered a best practice as it keeps your portfolio from drifting away from the risk profile that's right for you. But in a taxable account, rebalancing almost always means selling appreciated assets and paying capital gains taxes on the gains. That drag is easy to overlook, but it adds up.

Take a simple 60/40 portfolio ($VTI for stocks, $BND for bonds), starting with $100,000 in 2015, and invested over 10 years and rebalanced annually. The tax drag from rebalancing alone reduces the final portfolio value by $13,613, a difference of 0.65 percentage points per year.

If you have an annual giving goal, a DAF lets you rebalance and give at the same time, without the tax hit. Instead of selling your overweighted positions, donate them to your DAF. Then use the cash you would have given to charity to buy the underweighted assets. You've rebalanced, you've given, and you've sidestepped the capital gains entirely.

It's one of those strategies that sounds almost too good to be true, but the math works. For anyone with a taxable investment account and a regular giving habit, it's worth running the numbers.

It's time to open a donor-advised fund

If any of these scenarios sound familiar, getting started is easier than you'd think. With Daffy, opening an account takes less than a minute, and you can fund it with cash, stock, ETFs, mutual funds, or crypto.

The strategies in this post aren't complicated, but they do require having the right account in place before you need it. A windfall doesn't wait. Year-end doesn't wait. The best time to open a DAF is before the moment arrives.

If you give to charity regularly, these four strategies can add up to real money: a lower tax bill for you, and more resources for the causes and organizations you care about. Learn more about getting started with Daffy.

The information on this page is for educational purposes only and should not be considered tax or investment advice. Any calculations are intended to be illustrative and do not reflect all of the potential complexities of individual tax returns. Please consult a tax and/or investment professional to assess your specific situation.